I wrote a post making the argument that VAT is regressive in July 2010 because of the planned rise by the then new Tory government in VAT rates and the argument put forward by the IFS at the time that this was not a regressive act. I reproduce that post below. I do so because of comment on Twitter on this issue over the last day or two which might be summarised in this one exchange:

And:

Followed by:

And this:

The argument I published in 2010, which remains unchanged today, is as follows:

The UK government has proposed increasing the standard rate of Value Added Tax (VAT) from 17.5% to 20% from 4 January 2011.

They are not alone in proposing increases in VAT or equivalent taxes to address deficits in government budgets. The States of Jersey currently has a proposal to do much the same thing — increasing their rate of Goods and Services Tax (which is a VAT in all but name) from 3% to 5%. These rises will be contagious.

In this case though there is a curious link between the two proposals. A paper issued by the House of Commons library[i] on this issue and commentary in Jersey on the same issue[ii] both rely on work by the Institute for Fiscal Studies to support their claim that any increase in VAT is only mildly regressive at most, or might actually be progressive — as the IFS have claimed[iii].

A new Tax Briefing from Tax Research UK examines that Institute for Fiscal Studies claim and finds it is a statement of political dogma, but not of fact.

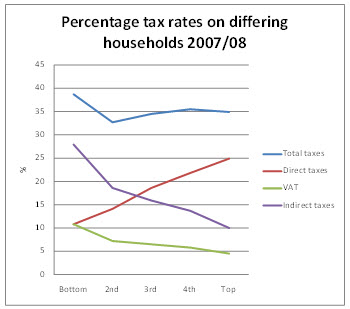

As the Tax Research briefing argues, a regressive tax is almost universally agreed to be one where the proportion of an individual's income expended on that tax falls as they progress up the income scale[i]. VAT is a regressive tax. This is shown, quite dramatically, in the graph below which is based on UK official data[ii] :

By chance the VAT and total direct tax burdens on the bottom 20% of households ranked by their income is the same. Direct taxes then rise steadily as a proportion of income as incomes rise and both VAT and all indirect taxes combined do the exact opposite, falling as a proportion of income as income rises. So marked is the trend that the overall progressive effect of income tax is not enough to counter the fact that the poorest households suffer such a high rate of overall indirect tax that they end up with the highest average tax rates in the economy as a whole.

The message from this data is unambiguous: the poorest 20% of households in the UK have both the highest overall tax burden of any quintile and the highest VAT burden. That VAT burden at 12.1% of their income is more than double that paid by the top quintile, where the VAT burden is 5.9% of income. VAT is, therefore, regressive.

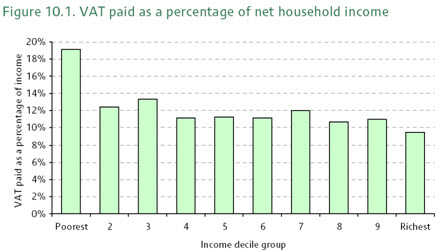

The IFS dispute this. They produce the following data in evidence:

They say of this:

It shows that the percentage of net income paid as VAT varies relatively little across most of the income distribution, with the biggest exception being that the bottom decile group does pay a higher fraction of its net income on VAT than do other income groups.

And they then use this claim to justify the fact that in their opinion VAT paid is not regressive with regard to income.

The slight problem for them is that this overlooks the very obvious fact that it is. Replotting their data and excluding the bottom decile as they would like the following graph can be drawn:

The linear regression shows a clear downward trend that makes very clear VAT is regressive.

Surprisingly the IFS ignore this obvious fact and go on to claim:

However, looking at a snapshot of the patterns of spending, VAT paid and income in the population at any given moment is misleading, because incomes are volatile and spending can be smoothed through borrowing and saving. Consider a student or a retiree: their current income is likely to be quite low but their lifetime earnings could be relatively high. The student may borrow to fund spending, whilst the retiree may be running down savings. Similarly, many people in the lowest income decile will be temporarily not in paid work and able to maintain relatively high spending in the short period they are out of the labour market. Because their spending is higher than their current income, these people will be paying a high fraction of their current income in VAT. Similarly, those with high current incomes tend to have high saving, and so appear to escape the tax, but they will face it when they come to spend the accumulated savings. Because of this ‘consumption smoothing', expenditure is probably a better measure of living standards (and households' perceptions of the level of spending they can sustain).

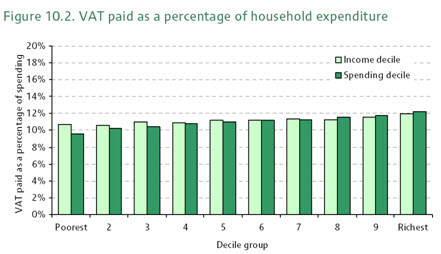

And they then claim that comparing VAT with spending shows that VAT is progressive:

However, this requires that a number of further conditions hold. First, the poor must have savings, and as I show, they don't. Second, they must have access to borrowing, and as I show, they don't (except for doorstep lenders). Third, the consumption patterns of the rich must be the same as the poor, and they're not. In fact, the consumption patterns of the rich (for school frees, private health, leisure travel, second homes and financial services products) are all VAT free, unlike the consumption patterns of the poorest. In addition, the IFS has to abuse all known notions of measure for progressivity to reach this conclusion.

The result is that far from the IFS claim being justified, it is vey obviously wrong, and very poor quality research. As a matter of fact VAT is regressive.

The IFS claim is, however, consistent with persistent IFS recommendations that VAT be increased (to replace corporation tax, for example, and on food and children's clothing to pay for “desirable tax reductions”) all of which, together with their recommendations that Inheritance Tax be abolished and tax on interest income be abolished suggest a systematic bias towards making recommendations that favour redistribution of taxes from those who work for a living or who are the poorest in our country towards those with wealth and who enjoy income from capital.

None of which makes it easy to see how the IFS can sustain the claim that [i] it:

maintain a rigorous, scientific approach to research, while offering scope for timely, independent, well-informed contributions to public debate.

The full paper is available here.

[i] http://www.ifs.org.uk/centres/esrcIndex

[i] It is, for example, defined as such in the Oxford Dictionary of Economics.

[ii] [ii] http://www.statistics.gov.uk/downloads/theme_social/Taxes-Benefits-2007-2008/Taxes_benefits_0708.pdf

[i] http://www.parliament.uk/briefingpapers/commons/lib/research/briefings/snbt-05620.pdf

[ii]http://www.gov.je/SiteCollectionDocuments/Tax%20and%20your%20money/ID%20FSR%20GREEN%20PAPER%2020100621%20MM.pdf

[iii] http://www.ifs.org.uk/budgets/gb2009/09chap10.pdf

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

richer people are also more likely to be registered for vat and able to use the reclaim to their advantage

rich people register for VAT so they can reclaim it on their purchases – wow what an incredible post, totally unevidenced and actually not possible.

Hobby businesses do get registered….

Agreed but that’s not what the allegation was. The implication was that rich people were able to reclaim vat on their luxury purchases etc which is not possible.

There are many items (useful and desired by all) which can be purchased by a `business` on which VAT can be reclaimed – and even purchase price offset against profits. This is one of the perks of being self employed (at whatever level) Anyone who thinks that this does not go on has no experience of commerce.

Of course trying to buy a Bugatti or a 54″ flatscreen telly on the business is a dead giveaway – but it still happens all the time : and with HMRC in such a mess it`s probably not a huge risk a lot of the time.

( For the record my car is 15 years old….)

anthony says:

“..rich people register for VAT so they can reclaim it on their purchases — wow what an incredible post, totally unevidenced and actually not possible.”

“actually not possible”. !!!

Nonsense. Of course it’s possible. Such ignorance delivered with such conviction. ! Staggering.

its perfectly possible to reclaim VAT on your louis vitton handbag. The issue crystallises when you have a VAT inspection and the Inspector asks exactly how the handbag is wholly and necessarily for use in your particular trade – at that point you start to get into rather sticky water.

anthony says:

“its perfectly possible to reclaim VAT on your louis vitton handbag. The issue crystallises when you have a VAT inspection and the Inspector asks exactly how the handbag is wholly and necessarily for use in your particular trade — at that point you start to get into rather sticky water.”

Well, yes Anthony, YOU might.

But I might be able to justify my Loius Vitton handbag quite easily. Perhaps you merely lack imagination…or style.

I wouldn’t keep my best spanners in anything less. 🙂

Neatly put. I noticed the creativity of a female pub owner decorating the pub with single expensive stilettos. Also by necessity certain activities require expenses eg Tour operators being paid to travel and stay, restaurant chefs dining out for research, landlords excess equipment storage, furniture stores write offs, greengrocers excess food, meetings of suppliers in Cannes or Haiwaii although I thought penalising weather presenters daily change of new clothes was harsh.

I remember when the tories hiked the VAT rate in order to reduce an even more regressive tax: Council Tax – but only to appease comfortable homeowners who had already been well served by abolition of domestic rates.

The focus on only one tax (in this case, VAT) seems quite misleading.

A better analysis would ask, what is the distributional effect of raising (or lowering) VAT compared with raising (or lowering) another tax, e.g. income tax, to achieve the same change in revenue.

Tax spillovers ….. which is what I am working on

You make an excellent point about the rich consuming VAT-free services like school fees, private healthcare, etc, and I would love to see how or whether more robust data including these services changed the conclusions of the IFS. However, is there not some benefit in looking at questions of tax progressivity for VAT from an expenditure basis rather than income basis? Measures of progressivity of a tax make more sense when you look at what is actually being taxed. So measure the progressivity of an income tax by looking at whose incomes are being taxed more (conclusion: the higher earners, hopefully); measure the impact of CGT by looking at which capital gains are being taxed, and measure IHT by looking at what wealth transfers are being taxed.

Surely measuring the progressivity of IHT by seeing what income beneficiaries were receiving would not tell you much, except perhaps that the children of wealthy parents also tend to earn high incomes. A more interesting measure for IHT would be to look at how much IHT individual fortunes paid over the long-term (i.e. taking into account lifetime planning, IHT reliefs, etc) rather than the income of the recipients.

The same can be said for VAT: is income really the best way of measuring whether a person is rich or poor? Surely expenditure is a more accurate measure, given that it cannot be faked: a person can only spend money they have, or money they have access to. Measuring expenditure is surely more effective at separating out the truly poor (those who are stuck in the bottom deciles with no access to historic, family, or anticipated wealth) and those that are only temporarily income-poor (e.g. younger people from wealthy backgrounds, asset-rich but cash-poor pensioners, people with volatile incomes with accumulated savings).

I appreciate that data for income is more plentiful than data for savings or lending facilities, but surely that is not a good enough reason to cling to income as the sole way of measuring a tax’s progressivity, particularly for taxes that do not tax income directly.

I am sorry – but expenditure can never measure whether a person is rich or poor

You ignore the balance sheet at your peril

And that is exactly what you are doing

This argument is just poor economic logic

Even the IFS graph (including the various flaws that you outline) that supposedly shows that VAT is progressive only just manages to do so! It’s desperate stuff.

“rich people consume a lot more”, yes, but not as a percentage of income!!!!!

I completely agree with you Richard, all the evidence is that VAT is regressive, and is one of the main contributors to making the UK tax system regressive overall.

The Economist also agrees:

“value-added taxes have been imposed on consumption, producing a welcome increase in the tax system’s efficiency but also making it more regressive.”

The Economist (in its recent anniversary issue!) is also saying that we need to make tax more progressive and tax wealth instead,

“tax regimes have lagged behind a changing world. Indeed, reform has often gone the wrong way. Over the past 40-odd years taxes on capital have fallen, as have income taxes on high earners.”

https://www.economist.com/essay/2018/09/13/the-economist-at-175

Your claim is irrefutable as you have shown.

I suspect people who disagree either haven’t looked into it or just arguing the toss.

Do you know if a similar study has been done on insurance premium tax? Which is one of the major tax increase by the Tory’s. (Up £3 billion since 2007/8 – the date of the percentage tax takes of different households chart).

https://www.statista.com/statistics/284349/insurance-premium-tax-receipts-collected-in-the-united-kingdom-uk/

I suspect IPT rate will be a tempting one for the chancellor to raise further.

The tax rise on insurance imposed by the Tories made my blood boil when it was brought in.

VAT to me is just a form of lazy taxation – just imposed and far too easy to use thoughtlessly. Labour appreciated that when they reduced VAT after the GFC.

BTW – I do love to see the IFS getting roughed up here. It is a thoroughly malign organisation that can only be described as part of the formal fake news/information network. The media takes them far too seriously.

I understand that VAT was introduced in the Common Market because it was hard for the French to dodge.

Carol Wilcox says:

“I understand that VAT was introduced in the Common Market because it was hard for the French to dodge.”

International socialism was never going to fly was it… 🙂

My view is that VAT can be progressive and regressive at the same time. The OECD has a mass of literature for anyone interested – e.g. https://www.oecd-ilibrary.org/taxation/the-distributional-effects-of-consumption-taxes-in-oecd-countries_9789264224520-en

Any conclusion that the VAT is generally proportional or slightly progressive does not

necessarily mean that the VAT, when considered in isolation, is a fair tax. Assuming diminishing marginal utility of consumption, a proportional VAT will still have a greater negative impact on the welfare of the poor than the rich. A proportional VAT may also have a greater welfare cost on credit constrained households than on those with full access to finance. However, these are not reasons to consider the VAT regressive. Rather, they are reasons to consider increasing the progressivity of the tax/benefit system as a whole.

A huge OECD (2014) survey broadly confirms the ‘it depends on how you measure it’ results from the previous smaller-scale studies: the VAT appears to be regressive when measured as a percentage of current income in all 20 countries studied, but is generally either proportional or slightly progressive (as a result of the impact of the reduced VAT rates targeted at goods and services particularly consumed by the poor) when measured as a percentage of current expenditure. I am thus prepared to be ambivalent on regressive/progressive and to insist on a system that looks to correct-prevent regressive outcomes.

It doesn’t really matter what you think: Rita is a highly respected academic, and, contrary to your claims, is also on the side of progressiveness. Your verbal attacks on her put you in the same position as Dan Mitchell and the Coalition for Tax Competition – albeit you are doing the same nonsense from the other side of the political spectrum. You probably won’t post this. But I’ll finish with one final comment: Rita earned her stature. You were given yours.

If you were so sure of your position, and the facts,why the anonymity?

All you are actually seeking to offer is abuse.

And for the record, no one who suggested replacing corporation tax with a destination based sales tax which is, in effect, a VAT to replace a tax on capital, as Rita did, is on the side of the progressives.

Vlad the Impaled

I heard a very posh private sector tax specialist on yesterday’s Radio 4 saying exactly what Richard is saying about destination tax (reinforcing for me why Rita is wrong).

As for your rather rude comment it makes no sense. Both Rita and Richard have by various routes been given their academic credentials and earned them. Those routes were chosen by the academic bodies themselves who awarded them. What’s the difference?

What exactly is your argument other than the cheap semantics you use?

What does ‘IFS’ stand for?

Inaccurate Fantasy Shite ?

I suppose this is another of those wondrous ‘independent’ think tanks, pretending to be authoritative, is it ?

Independent of what exactly is a mystery. Sense perhaps?…..objectivity?….statistical competence? …..integrity?

I’m surprised it is necessary to argue about this.

VAT is in effect a flat tax. A gallon of vehicle fuel costs exactly the same whatever a person’s income. therefore if the fuel is a necessity it is a regressive tax, end of.

The minimal increased consumption of running a more luxurious car is neither here nor there in relation to the disparity of incomes.

The same principle applies to anything else which is subject to VAT and would be regarded as one of life’s necessities. To argue otherwise is to demonstrate stupidity, or ignorance, or is simply deceitful.

One aspect of this debate which isn’t often mentioned is that the long-term shift in the UK personal tax system is from income tax to VAT (and National Insurance contributions). In 1979 basic rate income tax was 30%, and standard rate VAT was 8%. By 2011, income tax was 20% and VAT 20%. Whilst there have been a lot of other changes (in particular, NICs have increased markedly since 1979), in terms of basic/standard rates that looks more or less like a straight shift from income tax to VAT. VAT is regressive as a proportion of income and slightly progressive as a proportion of expenditure. *However*, the overall burden of income tax is much more progressive than the overall burden of VAT – whether measured across income or expenditure deciles. So, when people are arguing for a shift from income tax to VAT (this was the Thatcher/Howe argument in 1979 and also the Coalition argument in 2010), they are arguing for a more regressive tax system. That’s the reality of the situation and it is an important point to make.

Thanks Howard

Sorry – should have said income tax was 33% in 1979, not 30% (it was cut from 33% to 30% in the June 1979 budget).