The UK is expected to have GDP of £2,054 bn this year (table 4.1 here).

In current cash terms that is expected to grow to £2,116 bn the following year. That is a nominal increase of 3%. 1.5% of that is real growth. The rest is forecast by the Office for Budget Responsibility to be the result of inflation.

In April this year M4, which is the broad measure of UK money supply, was £2,356 billion. That M4 is greater then GDP is normal. It had risen by £45 billion over the previous year.

I make the point for a reason. That reason is to note that we need new money creation each year. Money can only be created in two ways. Banks can lend it. Or the government can create it by running deficits.

Right now the government is aiming for and achieving a current fiscal balance: it is balancing its books on day to day spending. It is borrowing for investment, but not to cover current spending.

The aim of Chancellors for almost a decade now has been to reduce borrowing to zero: in other words, to withdraw from new money creation.

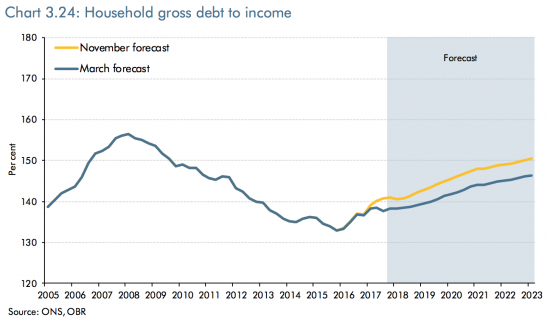

That means the private sector has to go increasingly into debt to fund the creation of the new money the economy needs. The risk of a private debt crisis is increasing as a consequence. This is the Office for Budget Responsibility forecast on debt from March 2018:

Debt stress is growing because the government will not be sharing the responsibility for creating the new money the economy needs by refusing to run the deficit that is necessary to create it. The result will be increasing financial vulnerability for millions of households.

Government financial irresponsibility does not get much bigger than that.

Deficit funding the NHS by £20bn a year could help rebalance this equation and help maintain the solvency of millions of households at the same time.

That is what a responsible government would do. But we don't have one of them.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Just watched James O’Brien of LBC on Facebook demolishing thr BREXIT dividend myth as funding for the NHS. O’Brien is one of the better journalists around but sadly he closes the rant with something to the effect that he still has one foot in the real world so the only place the money for the NHS can come from is taxation or borrowing. This is the magnitude of the task ahead when even the good journalists don’t get it.

It’s actually because businesses don’t trust banks any more. The flow of funds into business has died – even RBS admits it. How else do you explain 1/2% interest rates for so long? Government finds it excruciatingly difficult to unload bank shares. Toxic.

Read about Lloyds HBOS mistreatment of firms owned by Nikki and Paul Turner, and Noel Edmonds. Look at the firms RBS destroyed in recapitalising itself, classed as “Toxic” by Nicholas Macpherson at HM Treasury, and George Osborne.

Imagine you run a real business. Would you borrow “patient” capital from a bank which is going to try to get you into GRG (now called something else) within 18 months? I wouldn’t .

Hence dissatisfaction with government, Brexit, and Theresa May’s slap in the face at the polls.

All Treasury officials are Keynesians, and all push for this solution – spend your way out of trouble, just like Gordon Brown tried to do. Do you want him back?

With respect, your comments make very little sense.

First of all, people have no choice but use banks. They may not choose to leave their money there because the search for a return does not encourage cash holding, but that is an entirely different issue: that is the result of macroeconomic policy.

Second, most banks did not do what RBS did, even if I am not a big fan of many of them.

Third, the only major client base to withdraw from banking is not the one that you identified. It is, in fact, multinational corporations, most of whom now have their own internal banking facility, in effect, and do not, therefore, use the banks for this purpose anymore.

Fourth, if you think all Treasury officials are Keynesians then you are clearly deluded.

Fifth, nor was Gordon Brown a good Keynesian come to that. If you cannot differentiate types of economic policy then, again, what are you commenting for?

Harsh but true;o) Perfect answer.

I recall a couple of weeks ago you said that rollover of QE as bonds held by the BoE mature was worth about £20bn a year to the Exchequer. Does that count as deficit financing? I don’t think you could park it in one of the other categories of income e.g borrowing in the sense of from people who want a coupon, or tax receipts.

It’s a maintenance of the status quo: the amount of government created funding does not change.