Chris Giles at the FT had a good coronavirus crisis: his work on estimating real deaths was widely noted. But now he's back in familiar territory as a deficit fetishist under the headline:

As his article says:

Chancellor Rishi Sunak cemented his status as the government's Santa Claus on Wednesday, lavishing more gifts to help companies and households deal with the coronavirus crisis.

But while Mr Sunak hailed his “plan for jobs”, the bean-counters at the Treasury were totting up the cost to taxpayers. The chancellor's decisions in his summer statement, alongside plunging tax revenues, are likely to push the budget deficit up to £361.5bn, according to Financial Times calculations.

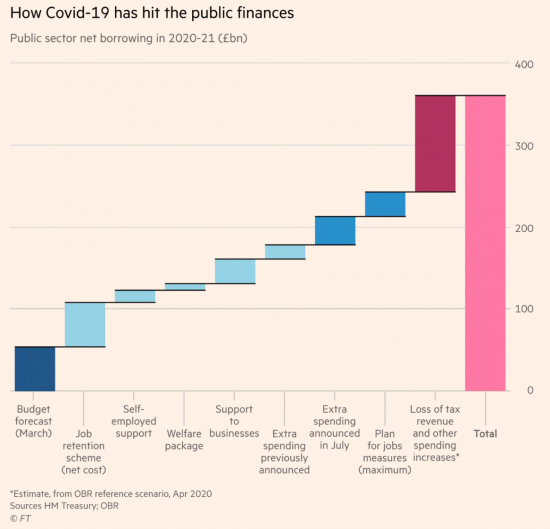

The usual range of good FT graphics are there to help. Start with this:

Which is a useful way of noting that so far nothing has been spent on rebuilding: everything is simply reaction to date.

Then note this:

And say 'so what?' followed by 'I bet it will be more than that before the year is out - because we ain't seen nothing yet'.

And then there is this:

This, of course, is a blatant falsehood since it ignores quantitative easing. If UK government 'borrowing' this year will be £361 billion, as the FT estimates, and quantitative easing will, we know, be at least £300bn then the real 'debt' has only risen by £61 billion at most, and not by £361bn the FT represents because the government simply owes itself the rest, which is meaningless. As a result national 'debt' is actually only about 65% of GDP.

But there is a more important question. And that is what is all this about? Giles says:

[T]he BoE bond-buying will not continue for ever, and Mr Sunak said he wanted to begin to “put [the] public finances back on a sustainable footing” in the autumn Budget.

Two questions: the first, is why can't it continue when it has in Japan for three decades and they still have not a clue how to create inflation there despite notional debt of well over 200% of GDP? And second, what is a sustainable footing? Surely, that's affordability, and we're borrowing at zero per cent right now. Issue it as perpetual debt at the same time, and the question literally goes away. So what does this paragraph by Giles mean?

And then there was this:

The chancellor will hope that the bulk of the deficit reduction will come from the economy beginning to fire on all cylinders again, but he is aware that he is likely to have to supplement this in the future through tax rises or spending cuts.

But Giles knows, as well as I do, that the economy is not going to fire on all cylinders again, and that even if it did that's the old and wholly unsustainable economy that needs £1 trillion spent on it via a Green New Deal to make it fit for the purpose of our survival as a planet. So this paragraph is meaningless. It isn't going to happen.

So what does Giles (and his fellow deficit fetishists) want? Is it people dying in the streets from hunger? Millions thrown out of their homes that they can no longer afford? A crushed NHS? A reduction in pensions? Children denied an education? An end to child protection? Which of these is that they will go for to create a 'sustainable footing' for the public finances?

And why do they want tax rises when they know these drain demand, and so jobs from the economy, simply increasing the economic crisis that we face?

Unless Giles says what he wants to do - and faces the real human cost of it - and says he can live with the destruction that it will create, all because he refuses to accept that a few taps into a computer at the Bank of England can continue to be made to deliver all the money that we need to prevent these catastrophes happening without any risk of inflation arising - then articles like this are meaningless.

But they're not without consequence. Because until he changes his tune Giles and the deficit fetishists are asking for people to literally die in the streets, having been throwing out of their homes because the government will have declared it can no longer afford them, or their healthcare, education or their protection. And these people need to be reminded of that.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

and the IFS is also asking “how the money will be paid back”?

is there any challenge by other economists to their status as the first oracle to be consulted?

It dies not matter what other economists say

The media have their contact books and they stick with them

It sounds to me as if they are going to win then?

I assume he is using Reinhart and Rogoffs 2010 paper that average annual growth was negative 0.1 percent in countries with episodes of gross government debt equal to 90 percent or more of GDP. This was later shown to be false as they made a mistake on their Excel spread sheet.

Is there any example of a government running a surplus when implementing a cut in government spending during a recession?

I doubt it…..

Mr Oldfield,

“Is there any example of a government running a surplus when implementing a cut in government spending during a recession?”

I cannot point to an example of what you seek, but I can point to an attempt to do so that spectacularly failed. It is a good illustration in the context of 2008, thinking of our predicament now, of just how catastrophically bad the economic management of Britian has been in the hands of the Conservative Party.

George Osborne tried to pursue a policy with the objective of achieving your outcome, with utterly disastrous consequences that led him, in spite of the bluster (see below) to change tack. The change of tack did not mean he gave up on a punishing regime of austerity on the disabled, disadvantaged and the Conservatives favourite target, the completely defenceless; but they did achieve ten years straight of economic stagnation, increased the national debt rapidly for no economic return return (save for 0.1% of the population who took everything and left us only a desert), and simultaneously completely and totally failed to demolish the deficit , or produce the intended surpluses. You could not think of a result that more completely failed to achieve anything at all – even the complete overhaul of the financial system. What we had was small scale, minimum change the City could escape with untouched; in short minor tinkering.

I quote excerpts from the Evening Standard, 25th January, 2013 – not without irony:

(https://www.standard.co.uk/news/uk/britain-heads-towards-historic-triple-dip-recession-as-economy-shrinks-03-8467040.html for full article)

“Britain is tumbling towards a historic triple dip recession, official figures revealed today.

The economy shrank by 0.3 per cent in the last three months of 2012 as the boost from the Olympics fizzled out.

The fall was worse than feared by many in the City and a hefty blow to Chancellor George Osborne’s economic strategy. Economists stressed that 2008-2012 was now the weakest four years of GDP performance in peacetime since the 1830s.

Amid the gloom, Boris Johnson [Mayor of London] called for the Chancellor to inject billions of pounds into London housing and transport infrastructure to inspire a boom and ignite recovery. Mr Osborne today said Britain is facing ‘a very difficult economic situation’ but is so far still vowing to stick by his austerity plans to deal with the debt crisis.He said: ‘We face problems at home because of the debts built up over many years and problems abroad with the eurozone, where we export most of our products, in recession. Now we can either run away from those problems or we can confront them – and I am determined to confront them so we can go on creating jobs for the people of this country.’

Britain last suffered such gloom in the Great Depression – but did experience difficulties in the Seventies, when the economy came very close to a triple dip recession, largely caused by the 1973 oil crisis.”

For Osborne’s not well hidden change of tack, see Reuters 20th March, 2015 – excerpts below:

(https://uk.reuters.com/article/us-britain-budget-osborne/think-tank-sees-remarkable-change-of-tack-by-osborne-idUKKBN0MG0JJ20150320 for full article:

“Chancellor George Osborne has shown a ‘remarkable’ change of approach on public finances, a leading think tank said on Thursday, a day after Osborne scaled back his austerity plans for the end of the decade.

Paul Johnson, head of the Institute for Fiscal Studies, said the eye-catching fiscal number in a pre-election budget announced by Osborne on Wednesday was a big cut to the size of a budget surplus in the 2019/20 financial year.

‘Of course surplus or deficit numbers this far in the future are of little interest in themselves — average forecast errors this far out run into the tens of billions of pounds, Johnson said at an IFS presentation.

‘But the apparent change in economic philosophy in the three months since the Autumn Statement is pretty remarkable.’

Osborne has made deficit reduction the central plank of his economic policy since he became finance minister in 2010 and he is urging voters in the May 7 national election to stick with his plan to restore Britain to financial health. But Fitch ratings credit agency said on Thursday it would be unlikely to restore Britain’s top-notch sovereign credit rating, lost in 2013, until government debt started to fall steadily as a percentage of national income.

In December, Osborne said he was aiming for a budget surplus equivalent to 1 percent of gross domestic product in 2019/20.

To achieve that, public spending as a share of GDP would have to fall to its lowest level since the 1930s, Britain’s independent budget forecaster said at the time.…

Osborne announced on Wednesday that the planned 2019/20 surplus had been scaled back to 0.3 percent of GDP, a lower target which did not draw such awkward historical comparisons.

The IFS comments, and Fitch’s refusal to consider a credit rating upgrade anytime soon, may add to the discomfort for Osborne after his latest tax and spending plans were described as having a rollercoaster profile’ on Wednesday by Britain’s budget watchdog.

The Office for Budget Responsibility said the squeeze on real spending in 2016/18 would be tougher than anything seen over the past five years. But that would be followed in 2019/20 by the biggest increase in real spending for a decade.

Osborne challenged the OBR’s description of his plan.”

Surpuses by 2020? Never heard of them. When neoliberalism actually hits a real problem, and not a mere oscillation of data within small margins, but something like a pandemic (a product of globalisation – that is just a fact); or an economic disaster brought on by neoliberalism itself, and its inability to regulate anything that controls wanton greed, or worse; or even wants to regulate its own wanton disregard for community interest: it just falls apart, and callson government – its nemesis – to bail it out; oh yes, and take no credit for anything.

Maybe it will cheer you up to know that the BBC Bitesize content on GCSE history covers the mistakes the government made on the economy during the Great Depression. Any of these look familiar?

https://www.bbc.co.uk/bitesize/guides/z34mwxs/revision/3

You could argue that it’s also deeply depressing that the most well known economists in our country aren’t even at a GCSE level on their knowledge of economic history.

Well spotted