Thankfully the Lib Dems have had the courage to do so. As the Guardian has noted:

The Liberal Democrats will highlight Britain's widening wealth gap during their conference after leader Sir Menzies Campbell insisted the party will hammer better-off families.

Deputy leader, Dr Vince Cable, will seek to take advantage of "genuine disgust" at tax dodging by the super rich to garner support for the party's policies to redistribute wealth.

Research carried out for the party indicates that 84% of the public believe the earnings gap between rich and poor is too large - with the figure rising to 92% among Lib Dem and Labour voters.

Some 72% think wealth inequalities have grown worse under Gordon Brown's stewardship of the economy, while two thirds want the richest to pay more tax, according to the poll.

I don't like the word 'hammer' at all. I also don't believe it. All most people want is a genuinely progressive tax system.

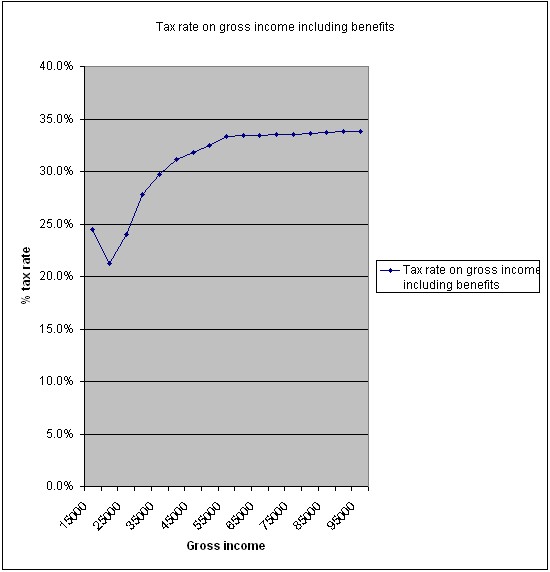

We haven't got that. Using national statistics data I recently produced this graph. It shows gross income including the value of state benefits paid in cash and in kind (mainly education and health) compared to total tax paid. From £55,000 on we have a flat tax in the UK.

There are three ways to tackle this:

1) A higher rate of NIC for those earnings more than £55,000

2) An investment income surcharge at, say 10% for those with investment income of more than £5,000 a year

3) A higher rate of income tax for those earning more than £100,000.

None of these hit middle income families as would, for example, removing top rate tax relief on pensions and as would simply abolishing the cap on NI contributions (bar 1%). If either of these were done the tax rate for those earning between £40,000 and £55,000 would become more progressive but the impact above that level would be more limited. My suggestions create increased progressively above that level. Which is fair, just and economically justifiable and appropriate.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

How about helping the poor person understand that they need to work harder.

I had a new temp employee come in and she was out the door before noon. Her excuse was that she was only interested in an entry-level job. We were more than wiling to train her but she wanted to do nothing more than answer the phones, and not too often.

Out of the 12 last temps, a full 7 were equally useless. It is surprisingly difficult to find people who actually want to work.

Punishing those who earn lots of money because others don’t feel like putting in the time and effort is is the wrong way to go. Stop handouts to the poor (with exceptions for those who really need it, suck as the elderly, infirmed, etc.) Choosing not to learn in school should not be rewarded. At the least they can be an example for their children to work in school.

Fred

Try treating those you employ as human beings of equal worth (if not equal pay) to yourself and then see how they respond.

I’ve always found it’s worked for me.

I’ve never seen contempt as a motivational tool.

Richard

Don’t mistake my attitude in the comment above for how I treat employees. I treat them like gold. Anyway, in the current job market in my area, employees can easily leave an abusive employer. (Not that I would if the job market was different.)

I am very patient with new employees because there is a steep learning curve and our goal is to work at their pace to allow them the time to learn the job. The job is not difficult but there is some learning involved. But the person does have to put in a little effort. This is where we find the problem.

I have had only three employees leave in the last two years. One finished nursing school and left for a nursing job. We permitted her to work two-years part time to do the school and the other just left to join a full-time nursing program. I currently have one other in a part-time MBA program. In every case I am very flexible to allow them to better themselves.

Your reply was very simplistic and fails to recognize that there are many people taking advantage of the system.

We hear a lot about the income gap and the wealth gap and what to do about the former – but never what to do about the latter. Why not?

People can be poor, in relation to others, not just because they are not good and conscientious workers, but because they inherit nothing during their lifetime while others inherit thousands, tens of thousands, hundreds of thousands, millions, tens of millions, hundreds of millions or even billions before they ever even lift a finger, given the unlimited gift and asset linked exemptions from IHT.

An annual wealth tax can only ever be a tax on the notional income from wealth, because higher rates would be confiscatory. It would be yet another measure to deal with the income gap – and not a very good one at that. We must recognise that the only time it is possible to do anything about the wealth gap – assuming we are genuinely concerned about it – is at the point of transfer from each generation to the next.

Inheritance Tax must be reformed in order to bring about in each succeeding generation a judicious positive redistribution of wealth that is neither created, earned, made or saved by beneficiaries – with a negative (receipt) and progressive tax on lifetime receipts of gifted and inherited capital. This would be the start of a new kind of popular capitalism to take the place of unbridled dynastic capitalism. Only The Liberal Party (not the EU-fanatic Liberal Democrats) – with British Universal Inheritance – and the Green Party – to a lesser extent – are talking about it. Is there a taboo elsewhere, hiding an uncomfortable but inspiring truth?

Dane Clouston

DANE CLOUSTON

Director, OPPORTUNITY – The Campaign for British Universal Inheritance

http://www.universal-inheritance.org

Land is one of the biggest depositories of inherited wealth, most often in the form of residential property but also as part of grand estates and vast agricultural acres. You don’t even have to use land to see its capital value increase by more than a working man’s yearly income. The historic landowners never sell land unless forced because they know it’s the safest way to hand down through the generations. It’s all held in complicated trusts, nearly half of UK land by acreage isn’t even registered. Trust funds never die.

This is totally unearned wealth and it could be easily taxed away by an annual land value tax.

We already have a Land Value Tax – in the form of residential and business rates, which just need to be extended to empty properties. But it is wrong to use it to “easily tax away unearned wealth”.

Not all land is unearned wealth. It may have been earned in the sense it has been bought with wealth that the owner, by luck, skill and the sweat of her or his brow, has created, earned, made or saved. Nevertheless, some land is unearned wealth, but then so are other assets – in the sense that they are received as gifted or inherited wealth that the beneficiaries themselves have done nothing to create, earn, make or save. The great thing about taxing receipt of wealth that is unearned in this sense is that the proceeds can be used for a judicious positive redistribution of wealth from rich to poor in each succeeding generation.

The socialist response to unbridled dynastic capitalism and its excessive inequalities is to wish away the private ownership of wealth. It is better for democracy and opportunity to spread wealth more widely with popular capitalism and ‘Inheritance for All’ in each new generation.

There are problems with inheritance tax. One is that often the recipient of land has to sell the land as that is where the value is trapped, or need to take out a loan on the land to pay the tax. It can be worse if it is a business or farm where the business needs to be dismantled due to the added expense of the tax.

On a personal level, I have seen my parents skimp and save. they have managed to pay off loans for their home and the home next to them. I keep telling them to sell and enjoy their wealth, but my father wants to leave it to his four sons so that we have it a little better than he did. (No, it is not any amount that would make him or his sons rich, but enough for him to life out his retirement in comfort.)

All an inheritance tax will do is encourage cheating or earlier transfer (In the US, parents can give children a set amount tax-free each year.) or just plain consumption and may even result in more elderly requiring public assistance as they rid themselves of all assets, at least on paper. Allowing the transfer of assets will encourage saving. this should benefit poor as well as elderly.

I wish people would research the issue before commenting on tax

Agricultural property enjoys very generous reliefs for Inheritance Tax menaing breaking up farms to pay this tax is not necessary in the UK

There are indeed problems with inheritance tax. For a start Inheritance Tax is not an inheritance tax. It is a cumulative lifetime gifts and bequests tax – a tax on giving and bequeathing from estates rather than a tax on receiving an inheritance. It is at a flat rate instead of at a progressive rate. It is at far too high a flat rate – 40%. It has, as a consequence, far too many exemptions.

Consider Fred Fry’s view at a personal level. His parents have managed to pay off loans for their home and the additional home next to them. His father wants to leave his wealth to his four sons so that they have it a little better than he did. (But what about those whose parents have died or have nothing left to give?) At present, if he takes no action, his estate will pay 40% on anything above £300,000, except for exempt assets such as land ‘in hand’. So, after exemptions, his four children will each pay 40% on receipts of anything above £75,000. Whereas if Mr Fry had only one son, that son would pay 40% only on anything above £300,000. Wouldn’t it better for tax to be progressive instead of flat – lower on small amounts received and higher on larger amounts received?

To avoid cheating there should be a tax on all giving of capital and another on all receiving of capital (however defined) so that there can be cross checking from one to the other.

As for definition of what is capital, it is not only in the USA that parents can give children a set amount tax free each year. In the UK I believe one can still leave £3,000 a year tax free, or £250 to any one beneficiary who has not received part of that £3,000, as well as gifts in the ordinary course out of income. Of course, what is income to some is capital to others, which is another reason for the twin taxes.

To avoid pressure for unwise earlier transfer that could leave parents requiring public assistance there should be a flat rate of 10% on the luxury expenditure of lifetime giving or bequeathing – on all of it – without exemptions for lifetime gifts or certain types of assets. So Mr Fry would come under no pressure to give anything away during his lifetime and therefore would have enough for him to live out his retirement in comfort. Any lifetime gifts he makes would be subject to the rates of the tax on receiving by beneficiaries. Of course, by not giving wealth away during his lifetime he will thereby increase consumption in order to live out his life in greater comfort. His son cannot have both concerns at the same time.

The Lifetime Capital Receipts Tax should be at progressive rates (starting at 10%) on gifted or inherited wealth that is unearned in the sense that the beneficiary has done nothing to create, earn, make or save it. With transferable tax credits between the two taxes to avoid double taxation, most people would have nothing to pay, since the 10% would already have been paid by/withheld from the donor. Beneficiaries of larger lifetime receipts would pay more tax. Donors would be encouraged to leave out the son who had already received a fortune from his fairy godmother.

Those receiving farms or businesses would indeed, if the donor or bequeather had not reserved against or insured against tax payable, have to sell a part of them, particularly if there was only one son rather than four and if he would be in a higher progressive rate bracket. However, it is not the end of the world for heirs of businesses or farms handed to them on a plate to have to borrow and earn back or even for the businesses or farms to be sold so that a number of children can share in the proceeds, or for part to be sold off if necessary. In any case there are always trusts if that is what is wanted, but it would be good to look more closely into that. Another reason for having the twin taxes, perhaps.

Allowing the unrestricted transfer of assets from one generation to the next will not necessarily encourage savings. Consider young trustafarians who spend rather than work and save.

At this point it should be asked what is the positive purpose of taxing the transfer of wealth from each generation to the next. The answer is that this is the only point at which it is possible to reduce the growing inequality of ownership of wealth and increase opportunity in our capitalist democracy. Which is why the cumulative Lifetime Capital Receipts Tax should be designed to bring about a redistribution of wealth in each new generation by being negative (a receipt of 10% of average wealth) as well as progressive (starting at 10%).

Average wealth of every adult and child in the UK at the end of 2002 was £85,000, according to the Office for National Statistics, as reported by The Times. I would, incidentally, very much like to know a more recent figure for this, but have so far been unable to get it out of the ONS.

DANE CLOUSTON

Director, OPPORTUNITY – The Campaign for British

Universal Inheritance

http://www.universal-inheritance.org