The government is claiming it cannot prosecute offshore tax evaders at present without proving intent on their part to evade tax if they omit information on their offshore bank accounts from their tax returns.

I have already said I do not agree. Nor do HMRC. This is the declaration on the 2013 tax return:

Now, let's think about this for a moment, shall we?

If the tax payer knows they have an offshore bank account on which income has been earned and they fail to declare it then very clearly they have evidenced intent to evade tax. What further evidence is needed of intent?

And if they don't declare it HMRC already say they can be prosecuted.

But HMRC say it's hard to prove intent and new law is needed. Self evidently both claims are wrong or the statement they printed on the 9 million or so tax returns they issued in 2013 is wrong.

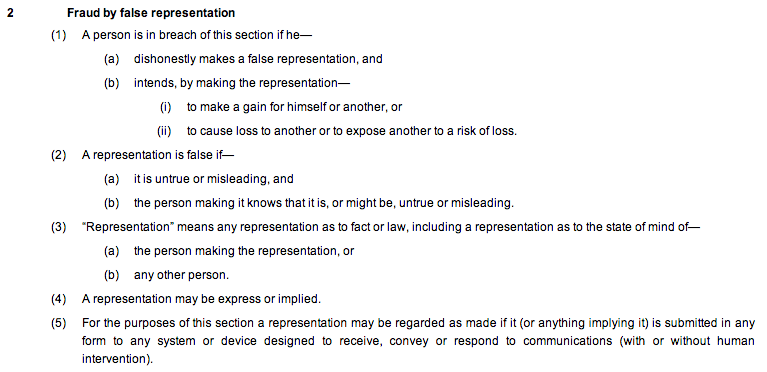

And what is the crime they can be prosecuted for now? It's simple: it's fraud. At one time it was called cheating the Revenue. The offence is described in section 2 of the Fraud Act 2006:

Everything needed to prosecute someone submitting a false tax return is there. The signature on a false tax return is the fraudulent declaration. The gain is the tax evaded. And I do it think subsection 2 is an obstacle: the requirement that the taxpayer appraise themselves of what must be declared is already imposed by law. Ignorance is not an excuse.

I make clear, of course I want prosecutions. I have been calling for them for a long time. But I cannot help but think that today's claims by Osborne, lamely defended by Gauke, look even more like posturing to me tonight then they did this morning.

My prediction is unambiguous: this new law, if passed, will change nothing.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

An interesting post. However, I think there might be some jurisdictional issues regarding the Fraud Act 2006.

I might be reading this incorrectly, but see this section from Blackstone’s Criminal Practice 2014:

“One consequence of fraud offences being ‘conduct crimes’ is that where D is guilty of fraudulent conduct abroad, with intent to deceive a victim within England and Wales, or with intent to gain or cause loss etc. within England and Wales, no constituent element of fraud is necessarily committed in England and Wales. The offence may be completed (and thus committed) entirely abroad. The CJA 1993, part I, applies English criminal law to transnational offences of fraud or dishonesty if, but only if, a ‘relevant event’ takes place within the jurisdiction – and the fraudulent obtaining of property etc. following a false representation or abuse of position etc. is not itself a ‘relevant event'”

It’s a UK tax return

Of course the misrepresentation is here

Let’s not be silly…..

Actually it might not be. Tax returns are submitted online and therefore the offence of making a false declaration could be committed overseas. Not a legal expert so have no idea whether this is relevant.

But it’s a UK tax return and w’re worrying about UK citizens

I really do not think submitting abroad is an issue

Or submission by an agent come to that

As I said, I’ve probably got the law wrong. I can’t though find any examples where the tax authorities have secured prosecutions under s 2 of the Fraud Act 2006 in respect of overseas undeclared income.

Maybe they haven’t tried

Maybe they have not got the resources to try

And maybe the willing has been absent

I think those the likely explanation

I think the phrase “… to the best of my knowledge and belief.” is also an issue. The prosecution has to prove to a criminal standard that the individual signed that declaration knowing the return was incorrect with the intent of making a gain. Given that an accused is, quite rightly, presumed innocent until proven guilty, that could be quite difficult if the only evidence is the incorrect return.

Why, when ignorance is no excuse?

Presumably a defendant can, and probably do argue, that they signed the declaration in good faith believing it contained details of all taxable income etc. The prosecution would need to provide convincing evidence other than a declaration that the individual knew that it was an incomplete return. Without such evidence, then you would be operating a strict liability position… which is where a change in law is required..

I repeat: I find that implausible

A wife signs her form, stating that she has no account with any money in it. Then they find the account. Well my husband has singed me up I know nothing.

Impossible

Accounts cannot be opened in that way

And marital coercion is now no defence

Really? Given how complex our tax code is, not to mention there will be offshore sources where it isn’t clear whether the return from those investments could be income, gain or return of capital, plus the information supplied will be complying with local laws not UK are you seriously saying it’s not possible for someone to submit an incorrect tax return in the genuine belief that it’s correct? I find your position implausible.

Making an error in disclosure is not the same as omission

Of course dispute happens – I am allowing for that

Oversight is another thing

And for the record – Redknapp was a claim there was no income

So it is possible for someone to submit an incorrect return with a genuine belief it’s correct.

On questions of law – yes

But there is ample room on the form to draw attention to such doubts

Dear Richard,

in my view and also due to my experience I think generally speaking we have the laws to prosecute abusive practice but those are not applied by tax authorities, prosecution and even judges. I have tried to make this clear with an open letter to the Head of Department of Justice and Home Affairs Mr. Martin Graf, Government Councillor of the Canton of Zurich last week. Here the link

http://liberte-info.net/docs/Rudolf_Elmers_open_letter_11-April-2014.html

The English of the letter still needs polishing and therefore please accept my apologies. However, the message is pretty clear I think.

The tax issue you refer to is similar or maybe even the same shortcoming in a judical system which we are made to believe should serve the society!

And the additional information boxes on the tax return are no doubt heavily used for that reason. The point is there will be circumstances where a person may have submitted an incorrect tax return and the onus is, quite rightly, on the prosecution to prove that the individual knew it was incorrect. If I was on a jury I’d find it difficult to convict someone if the only evidence presented before me was that the individual signed the declaration on a tax return that turned out to be incorrect. I would expect the prosecution to present at least some evidence that the individual knew that the return was incorrect at the time the declaration was signed.

Do you seriously think there is anyone who knows putting money offshore and not declaring it is legal?

Do you really take us for idiots?

Would it be a loose end though if one did not submit a Return at all?

Self Assessment is not a universal system and I know one should declare untaxed income in a Return but many 000’s of people already do not when they drift into higher rate tax with some investment income. Do you propose prosecuting them all for Fraud,or is there something particularly heinous about overseas income?

Not submitting a return when one is due is an offence already

I would personally have all submit returns…

Hmm, not Returns as they are. You almost have to be super intelligent to fill one out. I can barely do it myself, and I do it for a living. And what about the 000’s of people who are mentally disable or are semi Illiterate and don’t have the ability to fill one in?

Oh we’ll certainly have prosecutions. Now that the dressing is in place of the tax evasion window to gull the lame and dumb Liberal Democrats; the cheats, charlatans and conmen that run the Conservative party will move on to the task that they relish. No prizes for guessing what that is! Yes attacking the 21st century “witches” under the neo-feudal system, “benefit claimants” by ramping up the prosecution of “benefit fraud”. The work in progress of turning the legal system into the modern day “ducking stool” for claimants is well advanced!