Following Dave Hartnett's move to Deloitte I made an FoI request. The request and the answer are summarised here:

So, we now know people do leave HMRC to join the staff of the companies whom they previously taxed. And equally we know that until last year HMRC had no systems to monitor this potential abuse.

Both are worrying, but the practice the more so. How can it be allowed that HMRC staff can join the people they were previously taxing - taking with them their knowledge of HMRC's position on the company's issues? If that is not a revolving doors issue I am not sure what is.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Is there a risk that if you try to restrict movement from HMRC to industry/practice that people will simply not join HMRC in the first place, seeing it as too restrictive? Surely the last thing we want to do is disincentivise the ‘brightest and the best’ from considering a career in the civil service? (FWIW, I don’t buy the idea that there must be abuse when people move somewhere that they have connections; it’s dependent upon the morals/ethics of the individual – but I do agree that the current lack of transparency certainly fosters a perception of the possibility of abuse, which is in itself a bad thing)

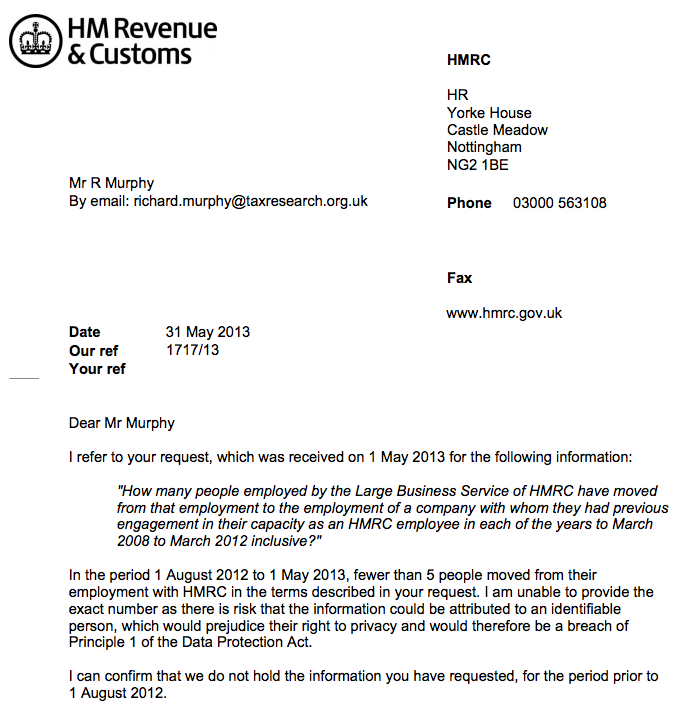

This admission is worrying in the extreme but not at all surprising. Furthermore, having sat and thought about their defense for not giving the exact number that too is highly dubious.

But leaving that aside I want to look at the other side of the issue. You rightly highlight that this allows HMRC staff to take priviledged knowledge and information with them and then use that in their new employment (unless HMRC staff are required to sign the Official Secrets Act, which as far as I know they aren’t).

But the other dimension to this situation is that an HMRC employee who intends to move employment in this way may well make decisions that are influenced accordingly, thus potentially improving their employment prospects, value, and so on.

This is such an obvious potential area for conflict of interest that we need to know what systems HMRC have in place to guard against such “temptations”. This is, of course, not simply an issue for HMRC, but for all government departments. But given HMRC’s role and responsibilities it is of fundamental importance that these safeguards are in place and that the public can have confidence in their effectiveness. Perhaps the basis for another FoI request? Certainly something the PAC needs to follow up.

“I am unable to provide the exact number as there is a risk that the information could be attributed to an identifiable person, which would prejudice their right to privacy and would therefore be a breach of Principle 1 of the Data Protection Act”

Isn’t it “wonderful” too how the Data Protection Act can be wheeled out to protect the powerful in the face of a public interest issue.

Should we substitute his for their?

Did “he” poach key staff for his new firm?

Hi Richard,

Sorry if I missed it elsewhere, what do you think to this?

http://www.telegraph.co.uk/news/politics/10102190/Donor-John-Millss-gift-to-Labour-avoided-tax-bill-of-1.5m.html

He did save tax

But is he allowed to give shares away, or not?

If so – where’s the avoidance?

I’ve never criticised arrangements within the spirit of the law

If gifts of shares rather than cash are specifically allowed (and I guess they are – if not I change my mind) then this is tax planning but a long way from being abusive

Not all tax saving is abusive, as I’ve long said

Sure, but that’s all a bit arbitrary on your part. Basically here you’re saying the law provides an exemption for gifting shares, so there’s nothing wrong. So I take it you’ve never campaigned to have the law amended to limit exemptions eg, CFCs?

It seems politicians have decided to grant an exemption, and that’s good enough for you Richard Murphy ….. in this case, anyway!

No

I have not said that – the motive test does appear to have failed here

But why donations to a political party must be in cash and not kind as you assume baffles me

If this were true for charities thousands o charity shops would be instantly out of business

It’s, effectively, a rather bizarre form of partial state funding of political parties. I have to say I’d be in favour of *proper* state funding of political parties, to reduce their dependence on wealthy donors like Mr Mills. For example, will the Labour Party now be swayed against introducing consumer protection legislation to ban many of the products, or many of the claims made for the products, that JML sell?

If I understood your logic I’d comment

I think there’s a misunderstanding of the tax benefit involved here. Donations (whether in cash or kind) to political parties are not tax deductible ….. after all, they’re not charities. I had assumed the tax benefit being talked about was gift relief from CGT (which he would have had to pay had he sold the shares and contributed cash proceeds to Labour). I appreciate the papers are talking about income tax rate savings (rather than CGT), but I suspect that’s just tabloid ignorance as usual.

So this was a classic example of Duke of Westminster in operation. His motive was to donate to Labour and to do so as tax efficiently as the law would allow. Not that different from the motive of some of those grasping corporates you rail against, of course!

But the gift made was specifically legal – there was no artifice

so is a lot of tax avoidance ….. doesn’t stop you railing against it

I am a proud trade union member and I work in local government.

I hope you can use your influence within the trade union movement to discourage HMRC or any employer from imposing such ties on employees, except in the most extenuating of circumstances, where the tie is kept to a bare minimum of clearly identified potential employers and the employee is very well compensated for giving up his/her freedom to work where he/she chooses.

It is unsurprising to me that HMRC do not (until apparently recently) have records of where their former employees now work. Why should the employees be forced to report their subsequent movements? It is none of their former employer’s (or anyone else’s) business.

Respectfully – yes it is if abuse follows

This practice of revolving doors – from government to industry and vice-versa – needs to be controlled if not eradicated. Not just for tax, but for all manner of govt services. Just look at what goes on in the area of defence in the U.S..

“Britain is now an increasingly corrupt country at its highest levels — not in the sense of directly bribing officials, of course, and it’s almost entirely legal. But our public life and democracy is now profoundly compromised by its colonisation. Corporate and financial power have merged into the state”

http://www.guardian.co.uk/commentisfree/2013/jun/04/corporate-britain-corrupt-lobbying-revolving-door

“But why donations to a political party must be in cash and not kind as you assume baffles me

If this were true for charities thousands o charity shops would be instantly out of business”

Just a little note on charities here: gifts to charities can be in any form they and the donor like. However, only cash donations qualify for Gift Aid. so the charity pretends – meaning lies – that it is acting as an agent for the donor in selling his goods for him. It takes a tiny commission to support this fiction/lie. After the sale it writes to the donor highlighting sale of his goods, referring to an earlier piece of paper the doner had signed when the goods were collected(!) and indicating that, unless he contacted the charity very shortly, it would be assumed he wished the charity to keep the money he was donating and that he also wished to gift aid his donation.

And yet that xharity is still writing to newspapers urging people to donate their goods; as opposed to their cash. This letter reveals the deceit, the fraud (not avoidance).

Why has this never featured on any blog called something like Tax Research UK?

I was unaware of that issue – if true

But it does not change in the slightest what I previously wrote. I referred to gifts in kind – which are indisputably legal

You deliberately missed the point

HMRC have always winked at this, and the rules on this we recently relaxed to make it easier for charity shops to claim the Gift Aid.

Although it was originally a fairly obvious case of tax avoidance, it’s now moved to being acceptable to HMRC.

So it’s not tax avoidance

Thank you

It used to be tax avoidance, but HMRC seem to have decided that it is acceptable.

In fact I would regard it as a perfect illustration of the principle that tax avoidance can be morally acceptable 🙂