The debt fetishists, like former Chancellor Sajid Javid, who are demanding that the government keeps borrowing under what they term to be control do so because they claim that there is a very real chance that current interest rates will rise.

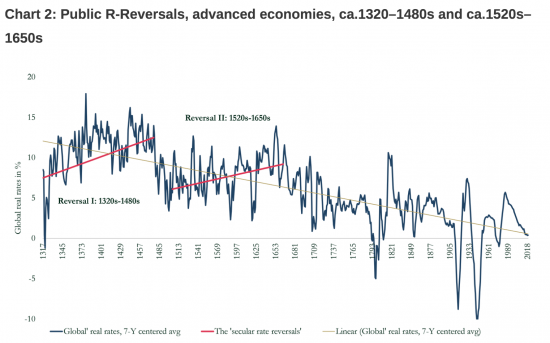

The Bank of England has just published a very interesting paper on this issue, looking at real interest rates in the world at large for the period from 1311 to 2018. Written by Paul Schmelzing of Yale University, this chart is, perhaps, the most interesting:

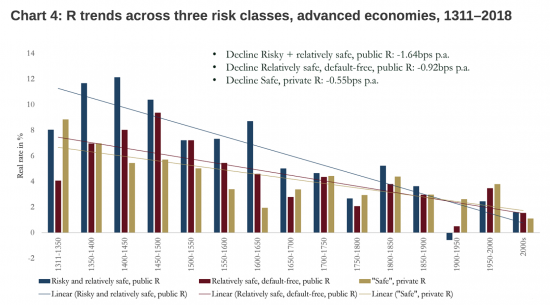

The background details are in the paper and I will not repeat them here. The critical point is that since about 1670 there appears to have been a continual overall downward trend in global real interest rates. As this chart shows, the trend holds true across a variety of types of debt:

Of course, this does not mean that there could not be short-term interest rate rises as a result of deliberate government policy decision. But what it does show is that this would be against all market trends, and therefore is highly unlikely to be sustainable. In other words, if anything, interest rates can still go down with much greater probability than they can go up, and negative rates looking increasingly likely for the long-term.

I stress, I am not offering these charts as proof of anything, but when the debt fetishists claim that interest rates will rise the onus of proof is definitely on them now, because the evidence is very heavily weighted against them, and we must always remind them of that.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

It would of course have to be Yale University and not one of ours!!

Does the over all drop in interest rates reflect the deep knowledge that debt is needed – that it is a positive think when large payments need to be made, that debt is more normal in other words than exceptional?

It also completely undermines the notion of monetarism as well to me at least, and this rubbish about leaving future generations indebted.

This is the reply to an e-mail from one of the MP’s that attended the Zoom meeting hosted by Angus MacNeil.

Pls can you offer a suitable response:

Thank you for contacting me about this. You are quite right that I participated in the Zoom meeting, and enjoyed Stephanie Kelton’s presentation immensely.

I agree with you that her ideas are very attractive in the current context……..I am little cautious about piling up the national debt, because one day interest rates will rise and the cost of servicing the debt could be a serious problem. Nevertheless, the ideas of Modern Monetary Theory should certainly be pursued, and I look forward to a chance to read Ms Kelton’s book.

Eric

Look at the post

And look at what Clive Parry has to say as well – including the fact that it would take ten years for our rates to really change and the trend is downward, the world over

The risk of interest rates rising is very, very low

You might be right and rates may stay low / negative forever meaning the 70s and 80s were a statistical oddity in th grand scheme of things. That said there are many items we all buy which have gone up significantly in price in the last 10yrs but they are not included in RPI or CPI. The question is really the debasing of currency whether it sterling g or whatever. Some feel that because everyone is printing/ debasing then it does t matter. Some feel it does. Hence the emergence of crypto and rise in gold. Whether the debasing of currencies continues or as you advocate is enhanced we can’t believe this will remain consequence free over the long term.

Hang on…..falling exchange rates because io Brexit is not the result of interest rates

You might want to check the date of the start of the significant decline in interest rates – nothing to do with Brexit.

Following the Brexit vote in 2016, rates were reduced by 25bps and then increased by 25bps TWICE soon after. The recent falls in rates were triggered by COVID-19, not Brexit.

You seem to have entirely missed the point.

Jen, the charts are showing real interest rates not nominal ones. The 1970s / early 80s might have had high nominal rates, but inflation means the real rates were usually negative.

True

Thinks: so that’s why my (nominal) salary increased rather a lot in that period.

😉

From a simple MMT perspective the growth in government involvement in economies, much of which has been to better balance their societies, has meant monetary sovereign governments creating much more money in their own right so “the price” of money (what interest rate can be demanded for it for loan purposes) will have gone down. The demise of the Gold Standard will have accelerated this. Also to be noted that many original MMT promoters believe base or bank rate should be held at zero and reliance placed on fiscal policy rather than monetary policy to regulate a country’s economy. Of course one can also argue that the resurgence of market fundamentalist Libertarianism is not unconnected with this given the rich especially like to make money on their savings as they sleep! (I’m sure Michael Hudson has something to say about this somewhere.)

I am not sure of the significance of this declining trend or why it is declining…. but here is a thought.

Investment requires financial capital AND human capital (with ideas and energy); without ideas/energy there is no demand to borrow money. So, why is the demand to borrow (NB. this is private borrowing, government borrowing doesn’t count) so low compared with the money available? Wealth and age…. which has increased over the centuries.

It is younger people that borrow and generate wealth. Older, richer folk want to preserve what they have so hoard cash.

What implications might this have?

First, what I say might be true in Western Europe but it is not true globally. Financial capital need to get to places that can use it.

Second, there ARE ideas in Western Europe that need financing (Green Deal etc.)….. but a lack of leadership/vision.

Third, old people hoarding cash for their old age will never be risk takers so government has to intermediate.

In conclusion, we DO have the human capital available (courtesy of COVID), we DO have the ideas (Green Deal), we DO have the financial capital (gilt yields at 0.5% for 50 years says so). We DON’T have politicians that understand this…. and this is true of Labour as well as the Conservatives.

A reversal of the trend of declining real rates would be indicative of a move in the right direction!

🙂

“A reversal of the trend of declining real rates would be indicative of a move in the right direction!”

What does this statement mean? Do you mean for both savers and borrowers? (For example, do you want to see the rate of interest on house mortgage loans go up?) When it comes to savers do you mean every saver including billionaires? (For example, do you think it’s a role of government to pay billionaires massive amounts of money via high interest rates on gilts?)

I raise this questions since I think there should be some protection against inflation by governments because they cannot be 100% effective in containing it but neither do I think there should be “blanket” protection.

I admit I am beginning to believe in differential interest rates – favouring small savers only

What I meant was that low real rates imply that we are not engaging in the crucial investment that we need. A rise in rates might be an indicator that we are finally investing in the Green Deal. better health care etc..

My assumption is/was that there is a single rate that all borrowers pay and all investors receive (give or take credit quality/maturity)….. and that means “winners and losers”.

You raise an interesting question about whether this is desirable…. no doubt, Richard might blog on this in the future.

But FWTW, I do think we need credit controls. It is wrong that equity speculators borrow at the same rate as home buyers and small businesses…… but I must confess, i have never thought seriously about differential rates for savers. I will now do so!

I will be returning to it Clive…sometime

…. and to the narrow point of the risk of rising rates.

First, look at Japan. The message is that rates are staying lower for longer than anyone imagined.

Second, the average maturity of UK Gilts is about 15 years. So, if/when rates do eventually rise we will have a decade or so before interest costs start to rise significantly.

Anyone scaremongering about higher rates really MUST be challenged.

Agreed..

The reasons for very low long terms rates in Japan are unique to Japan, the economics and demographics of the UK are quite different.

Different, of course

But not entirely so

There is still a glut of savings in the UK

Simply extrapolating the trend without understanding the reasons for that trend (and the current and possible future situation) is the stuff that a GSCE student would sceptical of.

To go on to say that the ‘evidence’ is that rates are more likely to go down than up is pure nonsense. We have a fully functioning forward rate market which states the exact opposite of what you claim.

Aside from a schoolboy trend line extrapolation, where is your evidence?

Tell me why you think rates will rise?

Which government is going to push them up?

And why?

Given that your forward market is merely punts on gov’t policy, tell us why, and what increase is forecast, over what period?

I agree, extrapolating trends is a dangerous game. However, I do speculate on the reasons for the secular decline in rates…… and that reason (older and wealthier population) is not changing anytime soon.

I agree, we do have a functioning forward rate market…. but be careful what you think that says. Par (swap) rates are what trades and are liquid, the forward rates are merely the arbitrage free rates derived from the par rates. They MAY contain some information rate expectations in the future but this is polluted by a lot of other factors (liquidity regulations, capital requirements, ALM issues etc.). All this “pollution” tends to make the forwards a biased (upwards) estimator for future rates and current market rates are perfectly consistent with the idea that rates will stay low for a long time.

Thanks Clive

I have just offered my three reasons for this, for what it’s worth

Richard,

interesting — why do you think that there has been a long term reduction in interest rates? Are these “real” interest rates and how accurate do you think the estimates are before the 20th Century?

The simple answer is risk has reduced and the quality of data to appraise it has improved

After that I suggest that capital has become more plentiful – at least as we currently define it

And third the willingness to hold it in debt and not take risk has increased – reducing the return on loans and bonds

That’s my short form response

The level of interest rates has to be related to the level of government activity in creating “money”:-

https://nathantankus.substack.com/p/the-federal-reserves-coronavirus

Thanks

“It may be shown, however, that the stimulation of private investment does

not provide an adequate method for preventing mass unemployment.

There are two alternatives to be considered here, (i) The rate of interest or

income tax (or both) is reduced sharply in the slump and increased in the

boom. In this case, both the period and the amplitude of the business cycle

will be reduced, but employment not only in the slump but even in the

boom may be far from full, i.e. the average unemployment may be

considerable, although its fluctuations will be less marked, (ii) The rate of

interest or income tax is reduced in a slump but not increased in the

subsequent boom. In this case the boom will last longer, but it must end in a

new slump: one reduction in the rate of interest or income tax does not, of

course, eliminate the forces which cause cyclical fluctuations in a capitalist

economy. In the new slump it will be necessary to reduce the rate of

interest or income tax again and so on. Thus in the not too remote future,

the rate of interest would have to be negative and income tax would have to

be replaced by an income subsidy. The same would arise if it were

attempted to maintain full employment by stimulating private investment:

the rate of interest and income tax would have to be reduced

continuously.”

Michael Kalecki The political aspects of full employment 1943

It is my opinion (I will take arguments to the contrary) that interest rates in the US, UK and anywhere that has had extensive QE, will not rise.

If you have a lot of money to save you can either put it into stocks or bonds.

As interest rates drop, the money that was in bonds moves into stocks.

Irrespective of what is happening in the “real world”.

Any move to increase the interest rate will reverse the flow of capital from bonds to stocks and the stock market will crater.

The putative reason for QE is to increase bank reserves to boost lending.

Banks are not reserve constrained, they are only constrained by the supply of qualified borrowers.

The real reason for QE is to immunise the asset holding class from the real world economy.

Ergo… interest rates will not rise.

Think Japan… but without the employment.

Am I right that Government bonds have the interest rate fixed for the whole term? (I know some might be inflation -linked , presumably not significant here). If so , what is the problem with interest rates rising in the future if interest payments (on most/all?) previous issued bonds will not be affected? If interest rates do rise in the future, then of course I can see that future “borrowing” will not be so cheap. Can’t we worry about that when it happens?

In your blog of 19th June, Richard, you say that since 2009, (what happened then?) the BofE has the ability to control and keep low both short term interest rates (via setting of reserve interest rates ) and long term interest rates (via QE). So is this not the definitive answer to interest rate fetishists? ie interest rates will be kept low by the BofE . End of. ? Is the fly in this ointment that the B of E may not necessarily want to keep interest rates low ?

I would be grateful, Richard , at some point, for a more detailed explanation (not here, necessarily) of how QE controls long term interest rates.

Jeff

QE, or rather the threat of it, keeps long term rates low. The government can always force the rate down.

And £700bn of central bank reserves means that the BoE can always keep short term rates low now – they totally control that rate

So why would rates rise?

Only because of inflation that can be controlled by rate rises? And where is that coming from?

The ignorance on this blog is astounding. The reason that the government is implementing QE is to keep Gilt yields lower than they would otherwise be in a free market.

If there was credible evidence that rates are set to reduce further, why are the BoE doing QE?

The ignorance on this blog comes from the right-wing commentators

The test of us know that the government sets rate and they’re not going up

See what I have just been posting

The OBR want part of the action, talking about the level of debt requiring austerity in the form of cuts in public spending or tax rises. And just to be really scary:

“even in its most optimistic scenario, public debt was on an unsustainable path and in the best case it was likely to exceed 300 per cent of national income by 2070.”

https://www.ft.com/content/a3ba1acc-5cf7-42de-86dc-176285af7715

Thanks for the heads up

I’d forgotten about it

[…] wrote yesterday that the chance of an interest rate rise is remote in the extreme. About 10,000 people have read that blog post […]