As the Bank of England announced in a report yesterday:

While most fixed-rate mortgages have repriced since mortgage rates started to rise in 2021 H2, the full impact of higher interest rates has not yet passed through to all mortgagors.

Over three million, or 35%, of mortgage accounts are still paying rates of less than 3%; the majority of whom will have their fixed rate expire before end-2026.

For the typical owner-occupier mortgagor rolling off a fixed rate between June 2024 and end-2026, their monthly mortgage repayments are projected to increase by around £180, or around 28%. Within that average, a relatively small proportion are likely to experience some very large increases – around 400,000 households will see an increase in their payment of 50% or more.

They published this chart in support of the data:

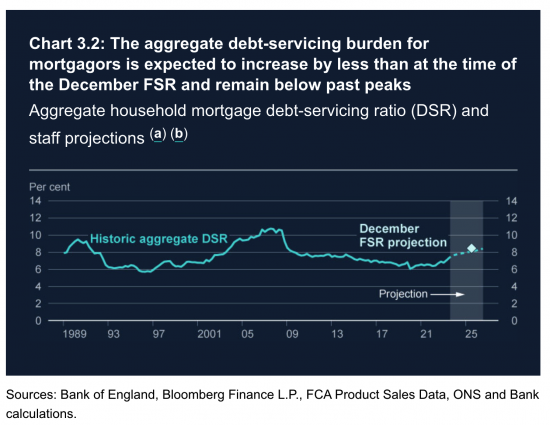

In the same report they produced this chart:

The message is clear. It is that, on average, the Bank of England think households are surviving wholly unnecessarily high mortgage costs, so they believe that those who have so far not suffered that pain should now be exposed to doing so.

They admit, they think mortgage rates might fall a little. But they offer no real comfort to anyone.

What is clear is that the beatings are to go on. We have clearly not suffered enough, although there is no hint that an increase in inflation is in any way likely at present (and if it happens, it will be world events, like the return of Trump, that will deliver it, and the UK interest rates will do nothing to tackle such causes).

Three thoughts follow.

One, good luck if Labour thinks this is an environment in which growth is going to happen. When a population is exploited by rentiers, they don't spend money to fuel growth.

Second, the bank is making the case for the end of its own independence. It is only the dogmatsim of Rachel Reeves that will save it.

Third, all of this feeds into the idea that we are living at the end of neoliberal times. A population who can see they are being exploited for no good reason will not tolerate it for long.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

I don’t really share your confidence there’ll be kickback I’m afraid. I need to explain why.

It’s said that a problem is merely a solution in disguise yet we appear to be largely a nation of trolls who don’t appear capable of seeing that a problem has previously been solved, solved in part, or not even recognise there is a problem. This is seen most clearly by those who do make the effort to think that none of the UK’s political parties are accurately and comprehensively identifying the country’s problems particularly in economic and monetary matters.

A good example of what I’m arguing is the government through its central bank paying interest on reserves. The existence of the closed system of government reserves resolved the problem of private or rather market based banks regularly failing and not able to meet inter-bank settlement requirements. The availability of government created reserves enabled “information-insensitive” money to always be available for borrowing for settlement purposes. Importantly government reserves provided a back-stop if other market banks wouldn’t lend to another market bank. A government reserves loan was always available but so was a discipline mechanism if a bank’s loans had been recklessly irresponsible the bank could be closed down or more rationally taken into temporary government ownership.

The question raised on your blog yesterday whether the government’s bank should pay interest on market bank reserve holdings is answered. It doesn’t have to spend money on maintaining a back-stop because the market banks can’t satisfactorily operate in the public interest without such a back-stop. If the government’s central bank doesn’t use base rate manipulation as a means of regulating the economy then the market banks would simply develop their own competitive rate range. Clearly a reluctance to lend by the market banks would be countered by government increased spending into the economy, Keynes 101.

We might have to differ on much of that

Unbelievable the arrogance of the BoE. We are still fighting the last inflation war and we have not inflicted enough pain on the mass of the population. Our aim? Continue the pain.

Utterly bonkers.

“A population who can see they are being exploited for no good reason will not tolerate it for long.” which is a fair point. But it raises the question – do they understand what is happening now & what might come down the track?

The politicos (Dogmatics Reeves & co – new characters in a Asterix book btw) have no interest in explaining this – their words show they are happy for things to continue – as is. As you note, the reckoning will come next year etc – far far too late – LINO well embedded & UK serfs back to being powerless.

Most people in the country know that there is a problem.

Most people in the country don’t know what the problem is.

Those with the influence have no interest in explaining what the problem is because for many of them it is not a problem.

If people understood the problem, I don’t believe it would be tolerated.